Question: Calculate the following ratios assume depreciation expense is $750,000 for both organizations

19 Aug 2024,10:30 AM

Presented below are financial statements (except cash flows) for two not-for-profit organizations. Neither organization has any permanently restricted net assets.

| ABC Not-for-Profit | XYZ Not-for-Profit | |||||||||||||||

| Statement of Activities | Unrestricted | Temporarily Restricted |

Unrestricted | Temporarily Restricted |

||||||||||||

| Revenues | ||||||||||||||||

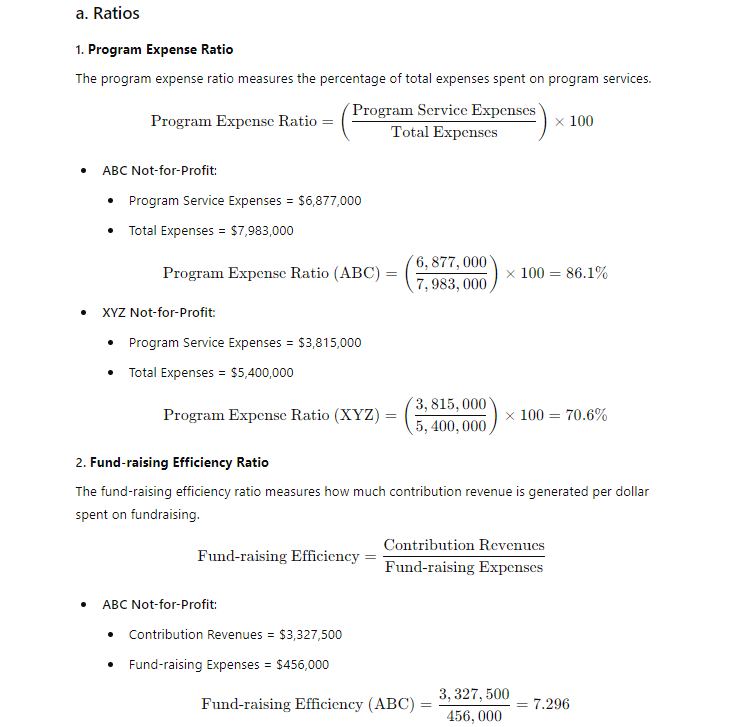

| Program service revenue | $ | 5,595,000 | $ | 2,250,000 | ||||||||||||

| Contribution revenues | 3,327,500 | $ | 750,000 | 3,200,000 | ||||||||||||

| Grant revenue | 96,000 | $ | 1,025,000 | |||||||||||||

| Net gains on endowment investments | 17,500 | |||||||||||||||

| Net assets released from restriction | ||||||||||||||||

| Satisfaction of program restrictions | 450,000 | (450,000 | ) | 377,000 | (377,000 | ) | ||||||||||

| Total revenues | 9,390,000 | 396,000 | 5,827,000 | 648,000 | ||||||||||||

| Expenses | ||||||||||||||||

| Education program expenses | 5,621,000 | 1,559,000 | ||||||||||||||

| Research program expense | 1,256,000 | 2,256,000 | ||||||||||||||

| Total program service expenses | 6,877,000 | 3,815,000 | ||||||||||||||

| Fund-raising | 456,000 | 356,000 | ||||||||||||||

| Administration | 650,000 | 1,229,000 | ||||||||||||||

| Total supporting service expenses | 1,106,000 | 1,585,000 | ||||||||||||||

| Total expenses | 7,983,000 | 5,400,000 | ||||||||||||||

| Increase in net assets | 1,407,000 | 396,000 | 427,000 | 648,000 | ||||||||||||

| Net assets January 1 | 4,208,000 | 759,000 | 1,037,500 | 320,000 | ||||||||||||

| Net assets December 31 | $ | 5,615,000 | $ | 1,155,000 | $ | 1,464,500 | $ | 968,000 | ||||||||

|

|

||||||||||||||||

| Statement of Net Assets | ABC Not-for-Profit | XYZ Not-for-Profit | ||||||||||

| Current assets | ||||||||||||

| Cash | $ | 205,000 | $ | 356,000 | ||||||||

| Short-term cash equivalents | 265,000 | 99,000 | ||||||||||

| Supplies inventories | 32,000 | 150,000 | ||||||||||

| Receivables | 439,500 | 188,500 | ||||||||||

| Total current assets | 941,500 | 793,500 | ||||||||||

| Noncurrent assets | ||||||||||||

| Noncurrent pledges receivable | 265,000 | |||||||||||

| Endowment investments | 2,590,000 | |||||||||||

| Land, buildings, and equipment (net) | 3,175,000 | 1,768,000 | ||||||||||

| Total noncurrent assets | 6,030,000 | 1,768,000 | ||||||||||

| Total assets | $ | 6,971,500 | $ | 2,561,500 | ||||||||

| Current liabilities | ||||||||||||

| Accounts payable | $ | 23,000 | $ | 129,000 | ||||||||

| Total current liabilities | 23,000 | 129,000 | ||||||||||

| Noncurrent liabilities | ||||||||||||

| Notes payable | 178,500 | |||||||||||

| Total noncurrent liabilities | 178,500 | |||||||||||

| Total liabilities | 201,500 | 129,000 | ||||||||||

| Net Assets | ||||||||||||

| Unrestricted | 4,025,000 | 2,364,500 | ||||||||||

| Donor restricted for purpose | 155,000 | 68,000 | ||||||||||

| Donor restricted for endowment | 2,590,000 | 0 | ||||||||||

| Total net assets | 6,770,000 | 2,432,500 | ||||||||||

| Total liabilities and net assets | $ | 6,971,500 | $ | 2,561,500 | ||||||||

|

|

||||||||||||

Required:

a. Calculate the following ratios (assume depreciation expense is $750,000 for both organizations and is allocated among program and supporting expenses):

- Program expense.

- Fund-raising efficiency.

- Days cash on hand.

- Working capital (expressed in days).

b. For each ratio, which of the two organizations has the stronger ratio.

(Assume 365 days in a year. Do not round intermediate calculations. Round "Program expense" answers to 1 decimal place and "Fund-raising efficiency" answers to 3 decimal places and "Days cash on hand", "Working capital" answers to nearest whole number.)

DRAFT/STUDY TIPS

Expert answer

This Question Hasn’t Been Answered Yet! Do You Want an Accurate, Detailed, and Original Model Answer for This Question?